The State of Alternate Protein in 2026

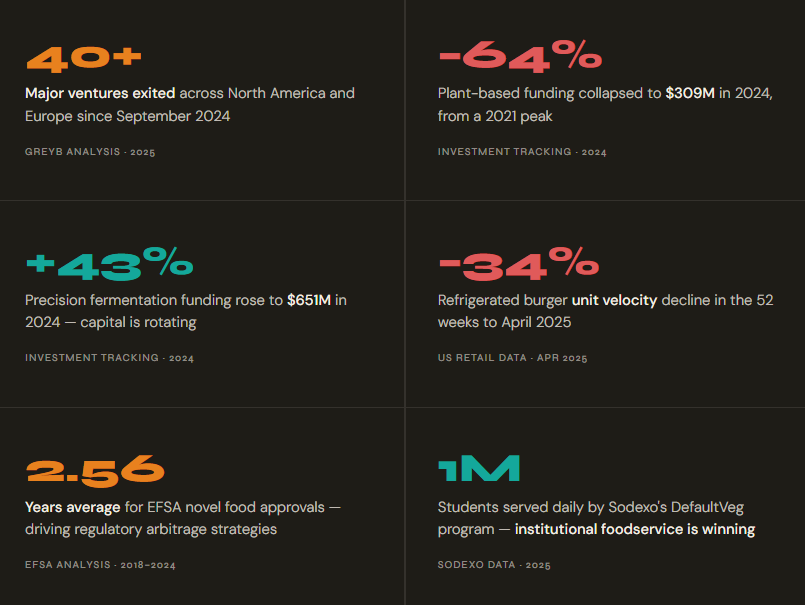

The alternate protein sector has entered a decisive consolidation phase. More than 40 major ventures have exited across North America and Europe since September 2024. Capital has shifted materially toward fermentation-led platforms. Retail velocity continues to decline across core categories.

For incumbents, ingredient suppliers, and investors evaluating exposure in this sector, the central question is no longer one of market potential — it is one of execution sequencing, partner access, and platform selection.

This report provides a structured assessment of where the sector stands operationally, where value is concentrating, and what the evidence suggests about durable competitive positioning.

What does the correction reveal?

The 2020–2022 investment cycle funded significant capacity expansion before three foundational conditions were established: validated unit economics at commercial scale, defined regulatory pathways across key markets, and demonstrated consumer repeat-purchase behavior beyond early adopters.

The resulting correction — visible through facility write-downs, covenant breaches, and company exits — has clarified the distance between announced capability and operational reality. It has also exposed which platforms carry structural advantages and which face structural constraints that additional capital alone cannot resolve.

The divergence is instructive. Quorn’s mycoprotein facility in Billingham has operated profitably at 24,000 MT per year across decades. Believer Meats’ $123M North Carolina facility secured dual FDA and USDA approval, yet ceased operations in early 2025 without achieving validated production. The gap between those two outcomes is not primarily a funding gap. It is a gap in manufacturing maturity, downstream processing expertise, and technology readiness.

Selected findings from the report

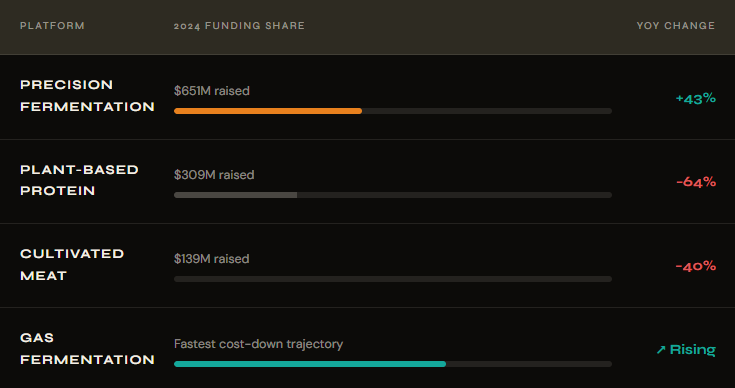

Precision fermentation attracted $651M in 2024, a 43% increase year-on-year, while plant-based investment contracted 64% to $309M and cultivated meat declined 40% to $139M. This capital rotation reflects a material shift in investor conviction toward platforms offering clearer routes to cost parity.

US retail sales of plant-based meat have declined for three consecutive years following a 2020 peak of $1.3B. Refrigerated burger unit velocity fell 34% in the 52 weeks ending April 2025. By contrast, institutional foodservice — operating through structured default-choice architectures — has demonstrated measurable expansion, with Sodexo’s DefaultVeg program serving approximately one million students daily across nearly 400 campus dining halls.

EFSA novel food approvals average 2.56 years from submission to publication. Singapore Food Agency and US FDA GRAS pathways offer timelines of 12 to 18 months. Companies capable of sequencing regulatory strategy across jurisdictions are reaching commercial markets materially faster than those pursuing a simultaneous global launch.

Access to commercial-scale contract manufacturing has become a binding constraint. The most significant CDMO capacity in North America and Europe is already committed to anchor tenants under exclusivity arrangements. ADM holds mutually exclusive rights to Air Protein’s commercial-scale gas fermentation plant. Liberation Labs’ 600,000-liter Richmond facility is fully committed to Vivici from 2026. Available capacity is concentrated in a small number of facilities, including Cauldron Ferm’s Queensland operation and Nova Plant Foods’ North Carolina plant.

Patent filing activity has begun to decline following a 2022 peak, with US filings down 37% year-on-year. The most patent-dense domains — texturization and basic scaffold design — present significant freedom-to-operate risk for new entrants. The least-contested areas, notably fat structuring and cost-optimized growth-media formulation, represent the most accessible opportunities for defensible IP development.

What the Report Covers

The analysis spans eight dimensions, drawing on operational data, investment flows, regulatory filings, patent records, and primary sensory research from 2022 through 2025.

Commercial Scale-Up Status: A comparative assessment of announced versus achieved production capacity across biomass fermentation, precision fermentation, cultivated meat, and plant-based ingredient platforms.

Competitive and Geographic Concentration: An examination of where innovation activity is clustering — across the Netherlands, Singapore, Israel, and the United States — and which regional conditions are proving most conducive to progression from pilot to commercial scale.

Retail and Foodservice Deployment: A structured analysis of performance divergence between open retail channels and institutional foodservice, including private-label dynamics across European markets and QSR retrenchment in North America.

Partnership Architecture and Supply Chain Access: A mapping of exclusivity arrangements, committed CDMO capacity, and upstream ingredient chokepoints that are shaping market access conditions for both established players and new entrants.

Regulatory Pathways and Market Access Barriers: A comparative review of approval timelines and requirements across Singapore, the United States, the European Union, Israel, Japan, and the UAE, including an assessment of beachhead sequencing strategies in practice.

Sensory and Functional Performance: A technology-by-technology assessment of the sensory gaps driving consumer attrition, drawing on 800,000 data points from the largest blind benchmarking study of plant-based meats conducted to date.

IP Landscape and White Space: An analysis of patent filing velocity and competitive density by technical domain, freedom-to-operate risks for new entrants, and the areas where first-mover IP development remains viable.

Failure Pattern Analysis: A structured examination of the five failure modes most consistently present across the 40+ venture exits recorded between September 2024 and August 2025.

Built for Decision-Makers

This report is intended for senior professionals evaluating strategic decisions in the alternative protein sector, including:

Innovation and R&D leadership at food and ingredient companies assessing platform risk, manufacturing partnership availability, and technical white space.

Corporate strategy and business development teams at food multinationals are evaluating acquisition targets, licensing opportunities, or co-manufacturing arrangements in a corrected market.

Supply chain and procurement leadership mapping ingredient sourcing constraints and the implications of upstream exclusivity arrangements for competitive positioning.

Download Report

51 pages. 8 dimensions. Zero growth-at-all-costs optimism. Get the operational intelligence your strategy actually requires.

Who are we?

GreyB is an innovation consulting firm which helps law firms, in-house IP and research teams, and business heads gain better clarity about their innovations, patent assets, and research challenges. They have expertise in analyzing patent data, understanding market dynamics powering research, and delivering IP consultations based on insights.

Facing A Roadblock

On Your Project?

Our Experts Are Here To Help.